Fixed Assets are held and used by a business for a longer period to be used in production, but these assets are prone to wear and tear or lose their usefulness over a period of time. So the fact here is that every tangible asset has a limited life. The only exception being land which is either held freehold or on a very long leasehold.

Think like this, you brought a new car for Rs 15,00,000 /-. After 2 years, the value of the car is not the same as you paid. For several reasons like usage, wear and tear, market value etc. the value of the car will decrease. The greater the number of years of use, the value keeps reducing.

Similarly, in business, the value of fixed assets should be adjusted so as to arrive true value of the fixed asset in financial statements.

In accounts, we recognize the value of wear out as depreciation.

Let’s say you brought a machine costing Rs. 1,00,000 /- which is expected to wear out after 10 years. This implies that the useful life of the machine is for a period of 10 years and post that, the value of the machine will be ‘0’.

Thus, every year you need to reduce the book value by providing a charge on the asset. You can do this by dividing the value of the asset by the useful life of the asset. This whole process is called depreciation.

In the above example, the deprecation charge is Rs. 10,000 /- (1,00,000 / 10) for the first year and subsequent year. For the 10th year, the value of the machine will be ‘0’.

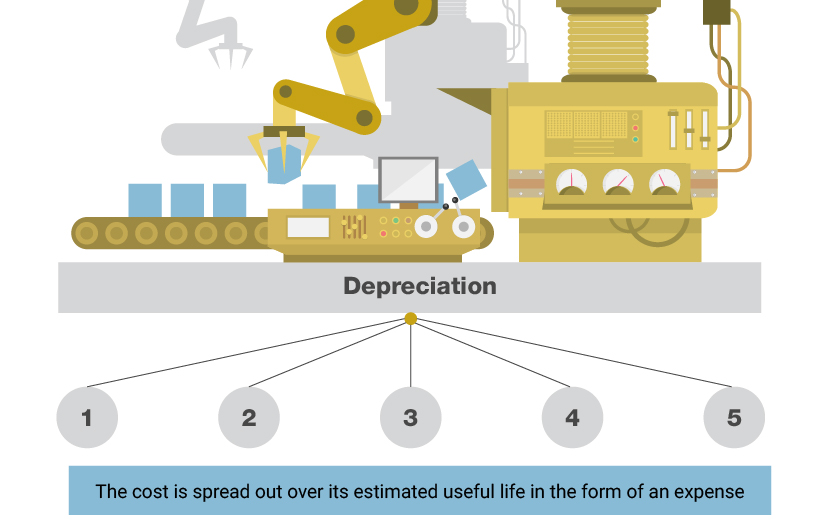

What is Depreciation?

With the above understanding, depreciation can be defined as a reduction in the value or the effective economic life of an asset owing to several reasons. The following are some of the key reason for depreciation.

- Passage of time

- Efflux of time even when it is not in use

- Wear and tear due to its use in business

- Obsolescence due to technological or other changes

- Decrease in market value.

As fixed asset has a life of over one year and it is expected to produce revenue over several years, it is important to spread the cost of the fixed asset over these years.

Depreciation in Balance Sheet and Profit & Loss Account

The depreciation charge in the profit and loss account represents the expense and can be viewed as the cost of using the fixed asset over the period for which the profit and loss account and Balance Sheet is prepared.

In the balance sheet, the assets are shown after reducing the depreciation. Some business show the full value of machinery (cost) in the balance sheet and then reduce the depreciation amount using a contra account. Read ‘Contra Account – Definition, Examples, Types and Importance’ to know more.

The concept of matching revenues with expenses in the year in which they are incurred are followed in accounting depreciation.

Depreciable Assets

To understand the assets which can be depreciated, let’ divide this section into 3 categories.

- Depreciable Assets Conditions

- Tangible Assets

- Intangible Assets

Depreciable Asset | Only if it meets the following criteria: -

|

Tangible Asset | Any purchased asset which can be seen or touched

|

Intangible Asset | Any purchased asset which cannot be seen or touched but has a value

|

The following assets cannot be depreciated:

- Land

- Current assets such as cash in hand, receivables

- Investments such as stocks and bonds

- Personal property (Not used for business)

- Leased property

- Collectables such as memorabilia, art and coins

Timeline of Depreciation

The depreciation accounting starts right from the moment the assets are placed in used and it ends when an asset is no longer useful, or it is sold.

![]()

- When the asset is placed in service.

- Ready and available for use in the business.

- When the cost of the asset has been recovered or when it is retired from service whichever occurs earlier.

- Example when the asset is sold or is no longer useable.

Depreciation Methods

The most common method used to depreciate assets are Straight-line method of Depreciation and Written down value method of Depreciation. The following are other depreciation methods:

- Sinking fund method

- Sums of the digit method

- Revaluation method

- Depletion method

- Machine hour rate method

- Replacement method

Comments

Post a Comment